“Rotation” Will become a Pipe Dream if the Tech Sector Declines in Any Broad Manner.

There are Some Real Cracks Emerging in the AI Phenomenon.

With next weekend being a long holiday weekend…and I will be traveling…we will not be sending a piece out. We may send out a very abbreviated piece Wednesday evening…if there is some sort of significant “new-news”…or a big jump in volatility…next week. Otherwise, we’ll be back to our regular schedule after the 4th of July……Thank you very much…and enjoy the holiday!

Table of Contents:

1) For the second time in four weeks, the tech sector fell 5% last week. What does it mean?

2) The groups we’ve have been bullish on continue to act very, very well.

3) South Korea’s stock market could be the canary in the coal mine.

4) The action in SoftBank’s stock is another candidate for the “canary” theme.

5) Updating the charts on the major indices….Different scenarios for each one of them.

6) Nice rebound in the Treasury market. Will an oversold oil market create problems for this rally?

7) The problems facing the private credit market are FAR from being over.

8) Bitcoin stands and an extremely critical support level.

9) Summary of our current stance…

Take advantage of our 25% discount to join The Maley Report….at this critical time in the markets!….This offer ends early next week!

---1) For the second time in four weeks, the tech sector fell by more than 5% last week. So, there is little question that this sector is starting to run out of steam. This does not mean it cannot regain its upside momentum going forward, but when you combine the loss of momentum…with some new cracks in the fundamental outlook…it raises some real questions about this all-important leadership group……Given how highly weighted it is in the SPX and NDX, a further decline in the tech stocks will make it very difficult for the recent “rotation” moves to continue in the weeks ahead.

Some meaningful cracks are beginning to appear beneath the surface of the technology sector…even though the long-term AI story remains intact in the eyes of most investors…..However, as always, it’s important to weigh both sides of the bull-bear ledger before drawing any firm conclusions.

On the bullish side, Micron delivered an outstanding earnings report last week…highlighting continued strong demand for its memory chips and reinforcing the view that AI-related infrastructure spending remains healthy……Under normal circumstances, that type of report should have provided another catalyst for the semiconductor group and the broader technology sector. Instead, however, the positive reaction was surprisingly short-lived. The sector quickly rolled over and finished the week lower, creating what looks very much like a classic “sell the news” response…..When markets fail to rally on good news, investors should pay attention.

That reaction becomes even more concerning when viewed alongside Broadcom’s recent earnings report….While Broadcom produced solid results, management failed to meaningfully raise forward guidance…leaving investors questioning whether AI-related demand is beginning to moderate……Taken together, the muted response to Micron’s excellent report…and Broadcom’s more cautious outlook could prove to be a “canary in the coal mine” for the semiconductor industry……This does not mean that a major reversal is imminent, but it IS enough to put it on investors’ radar screens.

Several months ago, software stocks began diverging from the rest of the technology sector as investors worried that advances in AI could make portions of the software industry less valuable. At the time, that weakness remained largely isolated…allowing semiconductors and the Magnificent Seven to continue carrying the broader technology sector higher. Today, however, the situation appears to be changing. The Mag 7 group has already slipped into correction territory…and renewed weakness in chip stocks raises the possibility that the deterioration is spreading across the entire technology complex.

The semiconductor group remains the biggest concern. Despite Micron’s impressive results, the SOX Semiconductor Index still declined last week. At the same time, the economics surrounding AI are beginning to evolve…..Many enterprises are shifting from subscription-based pricing…toward pay-as-you-go models, prompting companies to cap AI usage more carefully. That has contributed to falling input-token prices…and renewed questions about whether agentic AI can generate attractive returns at current cost structures. If token prices continue to decline…hyperscalers may eventually demand lower chip prices or increasingly substitute less expensive AI models (and there is some evidence that this is already beginning)…..Should this occur in any meaningful way, investors will begin asking much tougher questions about the long-term ROI from the enormous AI infrastructure buildout.

Again, none of this means the technology bull market is over…and more evidence is needed before raising a major warning flag. Nevertheless, both the fundamental backdrop and the technical picture (which we’ll discuss below) have become less convincing than they were just a few months ago.

Perhaps the biggest risk is what this could mean for the broader market. Sector rotation can work when technology is merely lagging…or even moving sideways…because capital can migrate into other areas while the major indices remain supported. Be that as it may, rotation cannot work in today’s marketplace when technology is actually falling. With technology representing a historically large weighting in both the S&P 500 and the Nasdaq 100 (over 35% in the SPX and over 60% in the NDX)…any sustained weakness in the sector would almost certainly pull the major indices lower as well.

If that happens, individual investors…who have become an increasingly important force in today’s market…will likely decide not to rotate into other sectors…but instead rotate into cash. This is especially true…given that they’ve been hearing bubble warnings for more than a year……….That is why the recent weakness in technology deserves close attention. It may prove temporary, but if it continues to broaden beyond software…and further into the Mag 7 (and especially into the semiconductors), it could become a much more important warning signal for the market as a whole.

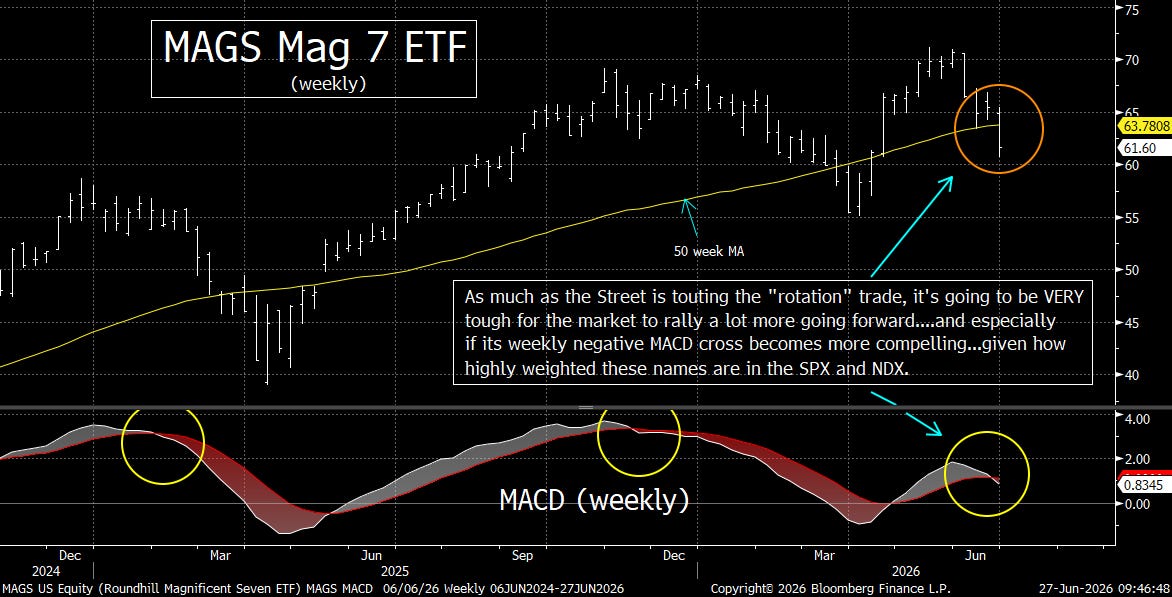

On the technical side of things, this is what we’re looking right now on the key tech ETFs/indices: For the MAGS Mag 7 ETF, it has already fallen into correction territory…and has broken below its 50-week moving average. It has been able to recover from a break below that line relatively quickly sometimes in the past, BUT the fact that it is also seeing a negative weekly MACD cross is a BIG concern. Those kinds of “crosses” have confirmed IMPORTANT changes in trend of the Mag 7 in the past. So, if the present negative cross becomes a more material one, it will definitely raise some serious warning flags. (First chart below.)

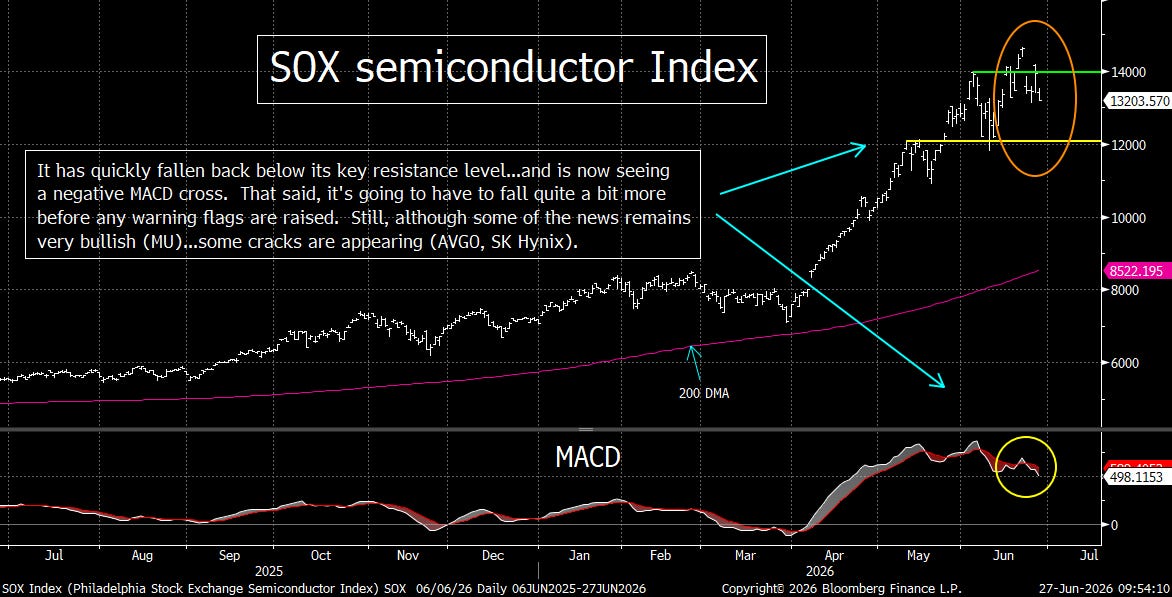

As for the SOX semiconductor Index, it dropped back below its key resistance level of 14,000…AND it has seen a negative MACD cross on its daily chart. This is not a significant development yet. It will have to drop below its all-important support level of 12,000 to raise an important warning flag on the chip group. Therefore, this group still has plenty of leeway. However, with the recent news out of Broadcom and SK Hynix, last week’s weakness is something that should not be ignored. (Second chart below.)

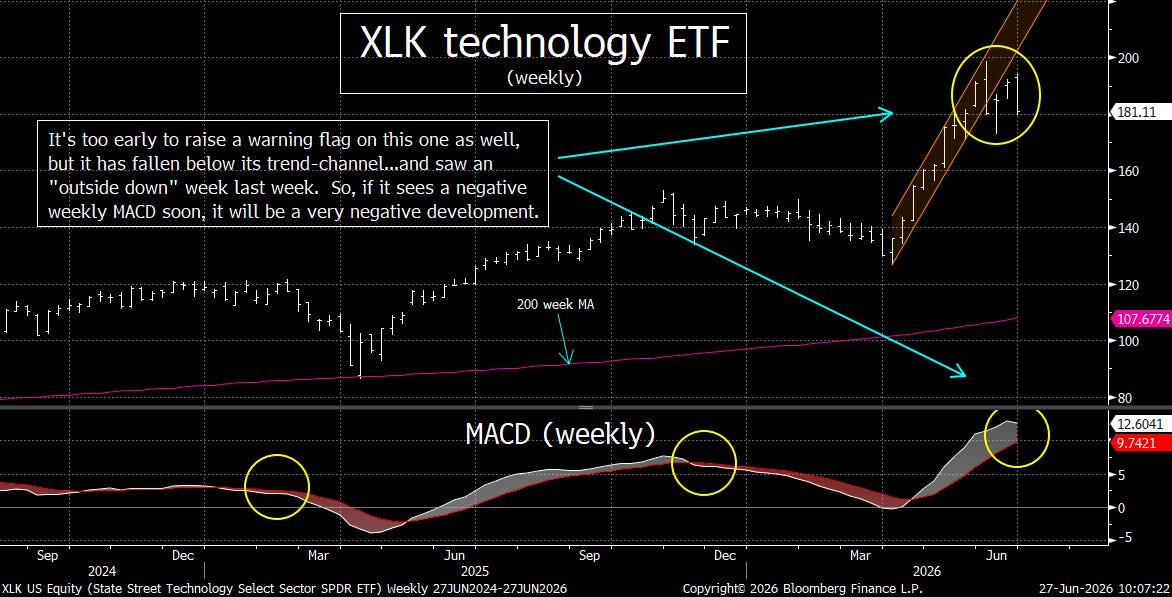

Finally, the chart on the broad XLK technology ETF is an interesting one as well. It has broken below its trend-channel from late March…and its weekly MACD chart is curling over (its daily MACD saw a negative cross earlier this month). However, that weekly chart is still quite a ways from seeing a negative cross, so it’s not an imminent issue right how. HOWEVER, the XLK did see an “outside-down” week last week…and that tends to be a compelling indication of a reversal in trend. Thus, it will be key for investors to keep a close eye on this chart as well. (Third chart below.)

It seems like that very time we see some cracks in the tech sector…like the ones we’re seeing now…the situation quickly changes back to the bullish side of things…and the sector (and the market) returns to its upward trajectory……Of course, this does not mean that the same thing will happen this time around…particularly since there are some fundamental issues which are starting to raise some questions. (In other words, it’s just the “froth” issue that is on investors’ minds.)….With this in mind, it will be critical for investors to watch this sector…and these groups within the tech sector…extremely closely as we move into the third quarter of the year.

---2) If the tech sector can avoid a further drop of significance, the “rotation” moves we’ve seen recently could indeed continue. There are some good fundamental reasons to think that the industrials and healthcare stocks can rally further…and the same might even be true for the material stocks…..Also, the industrials and healthcare ETFs are breaking out in a significant way…and it’s causing a lot of people on Wall Street to join us with our bullish stance on these groups.

After an extended period in which technology stocks have dominated the market…investors are increasingly beginning to rotate toward other sectors…including industrials, materials, and healthcare…….Several factors are driving this shift. First, there are growing signs of AI valuation fatigue…as many of the leading technology stocks now trade at historically rich multiples. At the same time, expectations that the Federal Reserve could maintain a more hawkish stance have caused investors to seek sectors with more reasonable valuations and stronger earnings leverage to the broader economy…..Also, the post-Iran ceasefire has also improved macroeconomic visibility, encouraging investors to broaden their exposure beyond the narrow group of AI leaders.

Industrials stand out as one of the more attractive alternatives. Companies are beginning to normalize inventories after several sluggish years…while non-AI capital spending is expected to accelerate by roughly 10% in 2026…following a 2% decline in 2025. That improvement could mark an important inflection point for U.S. industrial activity…with 2026 expected to be the first year of rising industrial production after three consecutive annual declines….Needless to say, continued data-center construction remains an important catalyst…while increasing adoption of robotics offers the potential for improved productivity and expanding profit margins.

The materials sector also appears well positioned. Demand for copper continues to strengthen alongside growing needs for electrical infrastructure…while paper and packaging markets are benefiting from improving industrial activity. Also, lithium demand remains supported by electric vehicle production…reshoring initiatives continue to boost domestic manufacturing…and strong demand for nitrogen and potash is benefiting agricultural markets……In addition, Project Vault’s proposed civilian strategic minerals reserve could provide another important tailwind for domestic producers.

Healthcare is also attracting renewed interest because of its defensive characteristics. Managed care companies are expected to recover following a difficult three-year underwriting cycle…while biotechnology firms should benefit from new drug launches and a potential pickup in merger activity. When you combine this… with the long-term demographic tailwind created by an aging Baby Boomer population…healthcare offers investors an appealing combination of stability and sustainable growth.

The technical outlook continues to improve for the industrial and healthcare stocks…but we do admit that there are some risks for the material names…...The XLI Industrials ETF is once again pressing against its February highs while also registering a positive weekly MACD crossover. It won’t take much additional upside follow-through to produce the decisive breakout we’ve been anticipating for several weeks. We turned bullish on the industrials well before the recent rotation began…and it now appears the rest of Wall Street is finally embracing that view. (First chart below.)

The IYM Materials ETF is a bit more challenging. It has pulled back over the past couple of sessions and is now testing the lower boundary of a symmetrical triangle pattern. That makes this an important technical inflection point. However, sentiment toward the precious metals has become extremely pessimistic…with bullish futures positioning falling to just 10% late last week. That leaves the group primed for a rebound…which could provide a meaningful catalyst for the mining stocks and…by extension…the broader materials sector. (Second chart below.)

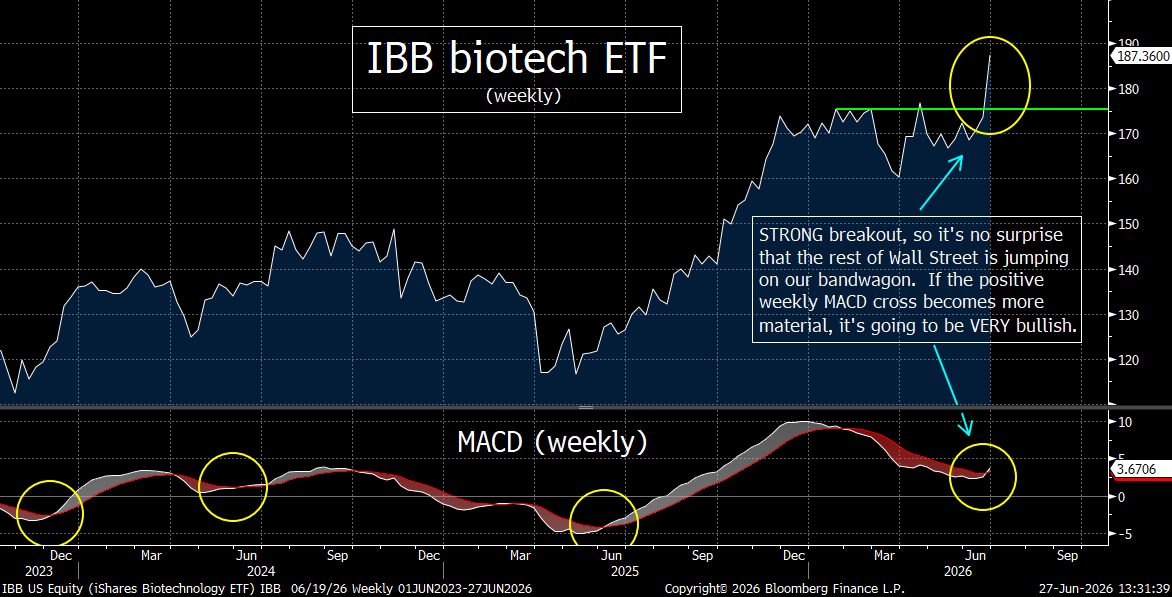

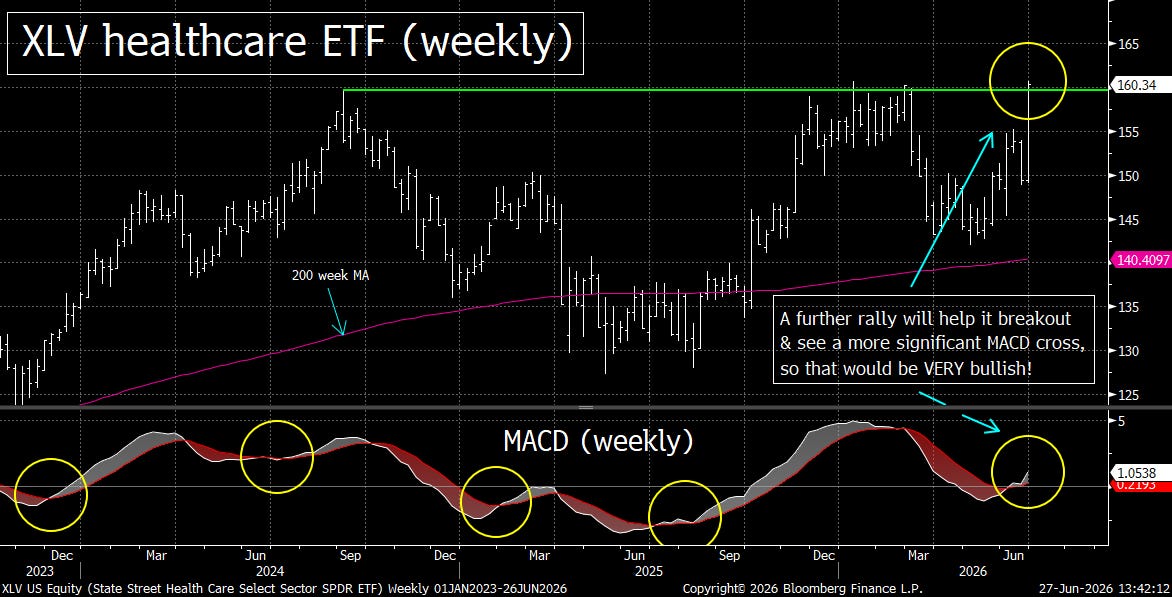

Meanwhile, the healthcare sector is also seeing a very strong rally…and it’s being led by the biotech stocks……Looking at the IBB Biotech ETF, it has broken out convincingly…and is beginning to see a positive weekly MACD crossover. So, if that “cross” becomes a bigger one, it will be even more bullish for this subset of the healthcare sector……As for the broader XLV Healthcare ETF, it is testing major resistance from last August, December, and March…while also registering a positive weekly MACD cross. Thus, a breakout above those levels would represent an important technical development…and confirm that investors are increasingly rotating toward the healthcare sector. (The third and fourth charts below.)

Finally, we’d just add that the individual stocks which we have highlighted from these groups have done extremely well since we highlighted them over the recent weeks…with last week’s additions (DE, VRTX, NTRX rallying further in a very nice fashion). As for the other sector that seems to be getting a lot of attention from the Street right now…the banks/financials…we’ll update our comments on them early next week. We’re not as sure as many others that this group will outperform going forward……However, we do feel confident that these other sectors will do well…if (repeat, IF) the “rotational” move we’ve seen recently can continue as we move into Q4.

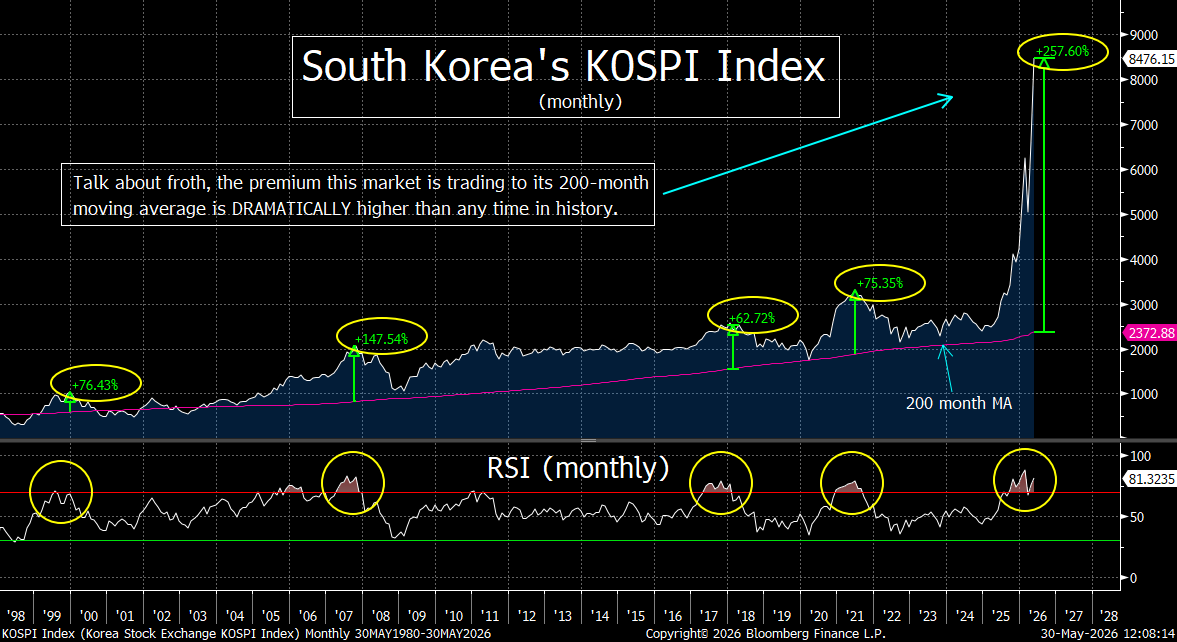

---3) The return of an extremely high level of volatility in South Korea’s stock market last week should have raised a lot more warning flags than they did last week on Wall Street. This market is extremely leveraged…and leverage works in both directions. Since the KOSPI index has become extremely overbought on an historical basis…and given the leverage in that market…any further decline could be an important canary in the coal mine for global investors.

We have always thought that South Korea’s stock market is one of the most important markets to watch globally…because their economy is extremely dependent on exports. In other words, its stock market is good indicator for its economy…and it’s economy is a good indicator for the global economy.

However, as we highlighted in our weekend piece at the end of May, the KOSPI has become even more important…and it could serve as a another “canary in the coal mine” for risk assets around the world……...While this stock market has enjoyed a strong rally over the past year, several underlying issues suggest that any renewed decline in the KOSPI could send an important warning signal to investors around the globe.

One of the biggest concerns is the extremely narrow nature of the advance this year. The rally has been driven largely by a handful of technology-related companies…most notably Samsung Electronics and SK Hynix. Market leadership has become so concentrated that when the Korean market reached a new 52-week high earlier this month…only 2.6% of listed stocks were making new highs…while an alarming 31% were already trading at new 52-week lows!!! Such poor market breadth often indicates that underlying conditions are far weaker than the headline index suggests.

Another major concern is leverage. Margin balances have surged from 23.3 trillion won ($15bn dollars) at the beginning of the year to roughly 38 trillion won ($24bn dollars) at the start of this month. However, when you factor in the broader credit and unsettled margin transactions, the number is closer to 60 trillion won ($39bn dollars)……This dramatic increase in borrowing has undoubtedly helped fuel the market’s advance. Too often, investors only blame leverage when markets decline…but leverage also magnifies gains on the way up. In other words, some of the strength in South Korean equities has been artificial…driven by borrowed money…rather than genuine investor demand. Thus, a downside reversal could turn into a very quick/violent one (more than we’ve already seen for far this month).

The leverage story extends beyond traditional margin debt. South Korea has become a global hotspot for single-stock leveraged ETFs and highly active options trading. These instruments can accelerate both rallies and selloffs…creating feedback loops that increase volatility. Recent market disruptions have highlighted those risks. Trading halts earlier this month…and again last week…have raised concerns that forced liquidations are becoming a growing problem. Some estimates suggest that roughly $6 billion of forced selling has already occurred…yet the unwinding process may not be complete.

If another significant decline develops in South Korea, investors around the world should pay close attention. A market characterized by narrow leadership…excessive leverage…and speculative positioning…often reveals cracks before they become visible elsewhere. For that reason, weakness in South Korean equities could prove to be an early warning sign for broader global markets.

As for the chart on the South Korea’s KOSPI index…we pointed out a few weeks ago that the KOSPI index had reached the same kind of overbought condition on its weekly RSI chart that it reached at the 2007 top (and more overbought than it was at the high in 2000). More compelling is the idea that it had reached a 257% premium to its 200-month MA…which is dramatically more stretched than any time in history! (First chart below.) We’d also note that although that market is trading at 24x forward earnings, it’s also trading at 1.8x sales. That is 50% higher than it was at the 2007 high!!!

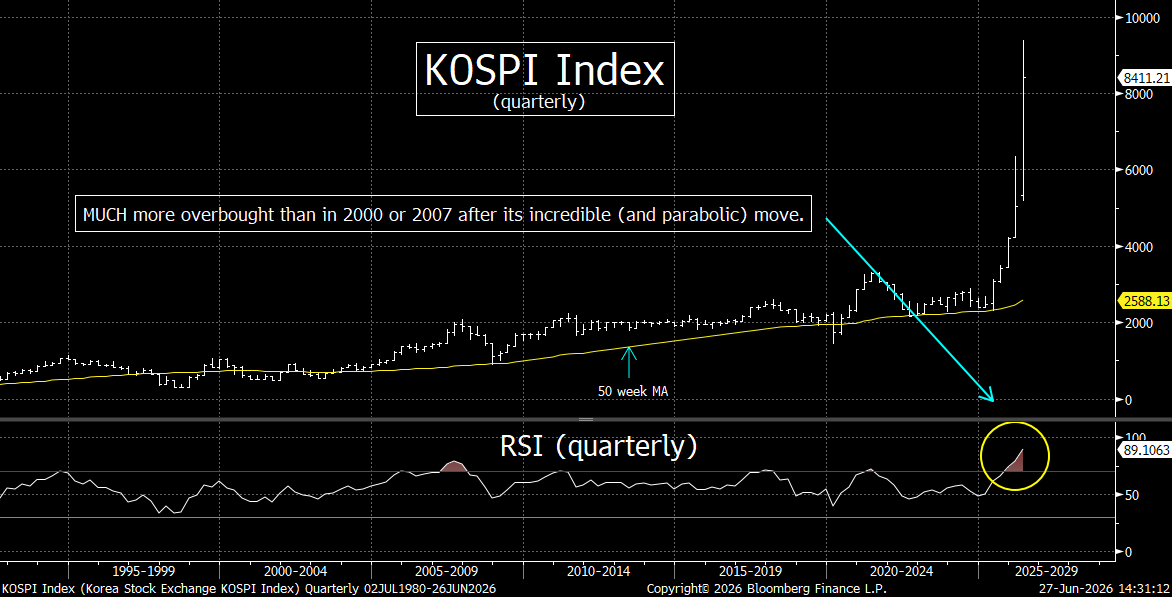

On top of all this, if you look at the very-long-term chart, the KOSPI is now trading at its most overbought reading on its quarterly RSI chart (by a very wide margin)…and it is trading FOUR standard deviations above its 20-quarter MA. (Second chart below.)………..Now, we readily admit that we don’t usually use quarterly charts…but this does show just how stretched that market has become…especially when its weekly chart is coming off such an extreme reading as well.

---4) SoftBank’s recent struggles could become a much more important issue for the technology sector…and the broader stock market than many investors currently appreciate. While AI remains one of the most compelling long-term investment themes…the market has a history of confusing an exciting secular trend with the short-term valuation of the companies tied to it. Those are two very different things.

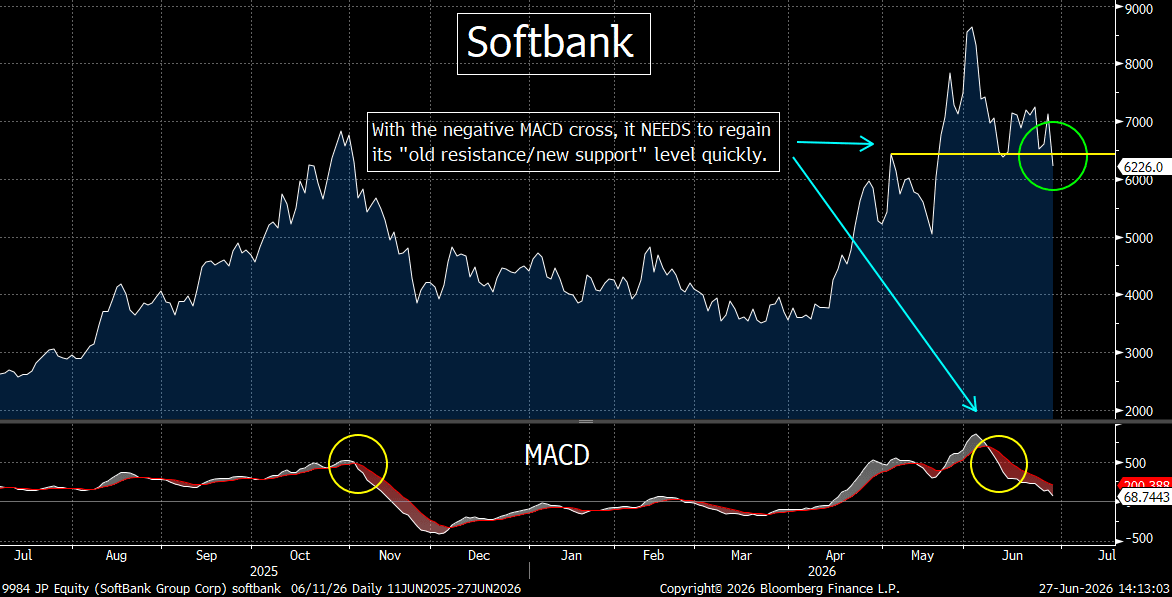

As we discussed in our daily piece on Friday, the action in SoftBank during the month of June has been very weak…and this could be a canary in the coal mine for the AI stocks going forware…..At SoftBank’s recent annual meeting, CEO Masayoshi Son declared that artificial intelligence is still in its infancy…and argued that any suggestion of an AI bubble was, in his words, “an insult to AI.” We certainly agree that AI is likely in the early stages of a transformational technological shift. However, that does not automatically mean that every AI-related stock is reasonably valued. Many of the sector’s leaders have already enjoyed extraordinary gains…and several appear to have become stretched from both technical and valuation perspectives. (As an aside, we also found it amusing that Mr. Son suggested AI could somehow feel the human emotion of being insulted.)

Instead, investors should ask whether these comments were,…at least in part…an attempt to defend SoftBank’s own shares. The stock has fallen nearly 28% since June 2 and is beginning to suffer meaningful technical damage. That weakness is important because it has been reported that roughly 60% of SoftBank’s investment portfolio is tied to AI-related assets…including its major stakes in Arm, OpenAI, Stargate, and numerous other AI ventures. The company also continues to carry significant leverage…making investors increasingly sensitive to any deterioration in the value of those holdings…..Concerns were heightened further late this week after reports that a potential OpenAI IPO could be delayed, adding another headwind to sentiment surrounding the company.

The technical picture has also deteriorated noticeably. SoftBank had fallen below the important support provided by its October highs from last year (it’s “old resistance/new support” level) early last week. Then, Friday’s sharp 12.5% decline also pushed the stock beneath its uptrend line that had been in place since April while creating a decisive “lower-low” below the mid-June low! Perhaps most concerning, the shares are not yet oversold despite the sizable decline…suggesting there could still be room for additional downside before bargain hunters begin to step in.

Given SoftBank’s enormous exposure to the AI ecosystem, its stock could become an important barometer for investor confidence in the entire AI theme during the second half of the year…….If the shares continue to break down, it could signal that enthusiasm for AI-related investments is beginning to cool. That would not necessarily mark the end of the AI revolution, but it could mean that expectations…and stock prices…have gotten ahead of themselves…creating a meaningful headwind for technology stocks and the broader market in the months ahead.

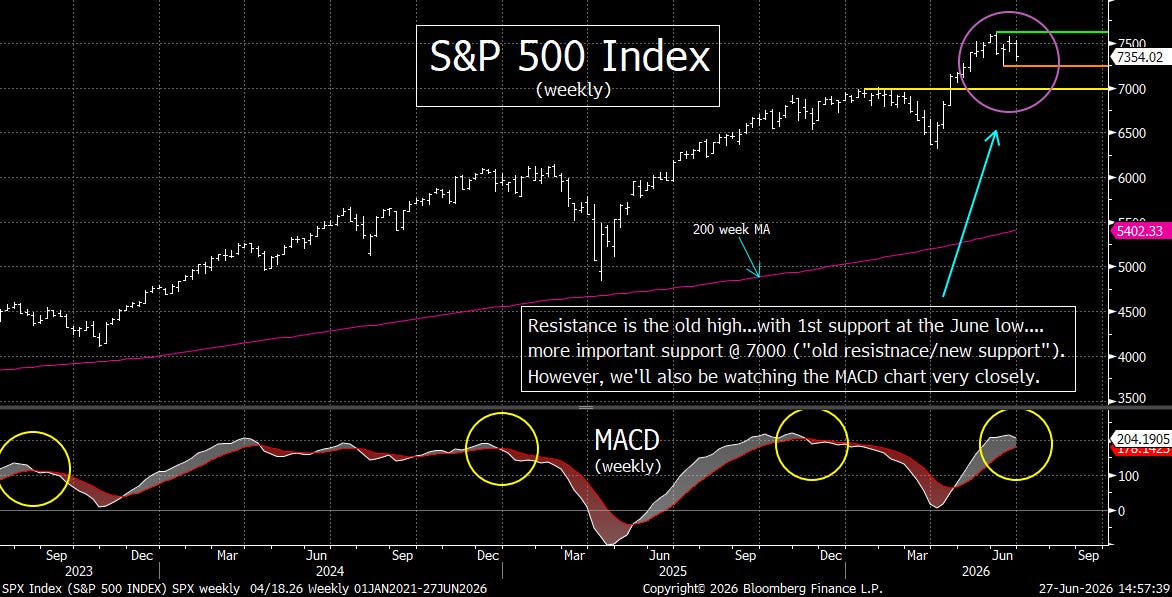

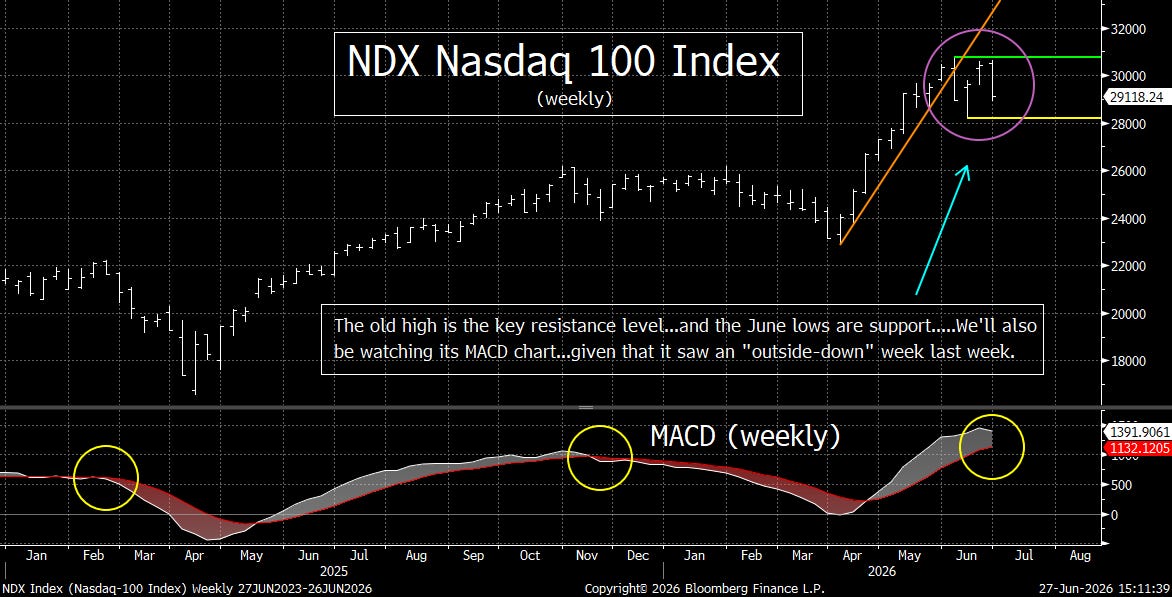

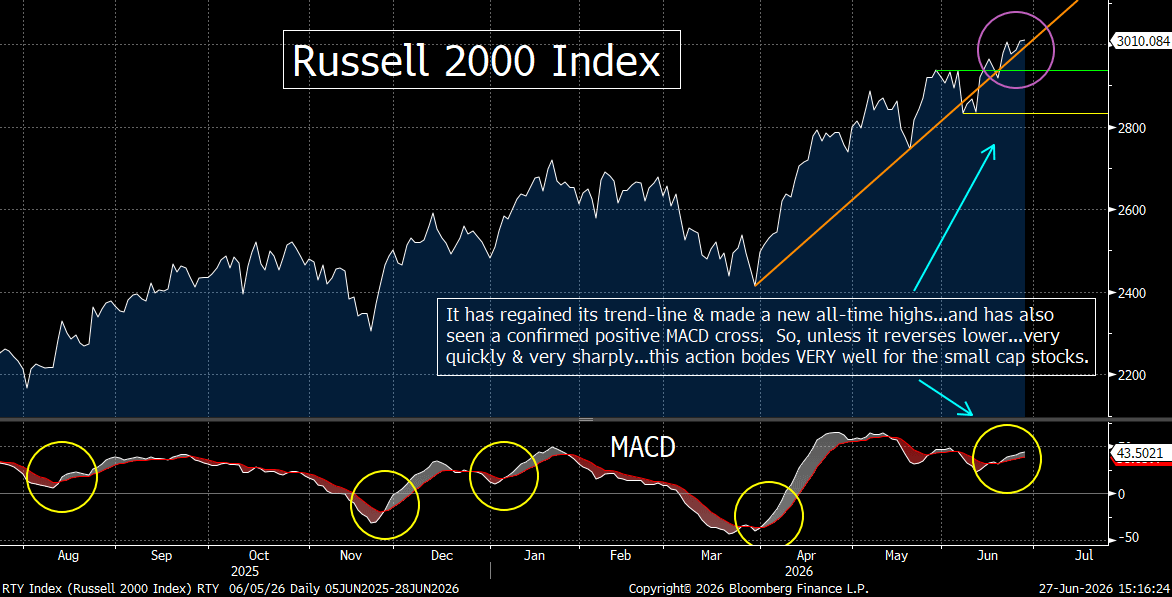

---5) Index charts………As we head into the end of the second quarter…and prepare for the start of the third quarter…the charts of the major stock averages are sending a mixed…but very interesting, technical message. The S&P 500, the Nasdaq 100, and the Russell 2000 are all showing different characteristics…making it especially important to analyze each one on its own merits rather than treating the market as a single entity.

Starting with the S&P 500, the weekly chart remains constructive…but it has failed to produce the decisive breakout that many investors were hoping to see. (Thus, that old high of 7,600 remains the key resistance level.)…….That said, last week’s pullback was relatively modest and, importantly, the index continues to hold comfortably above its June low at 7,267… which represents the first meaningful support level. The more critical level, however, remains the 7,000 area. That was the major resistance level from earlier this year before the market broke above it in April, and so that “old resistance” has become “new support.”….. As long as the S&P 500 holds above that level…the longer-term technical picture remains intact.

We are also watching the weekly MACD closely. Although it has begun to curl lower…it has not yet generated a negative crossover. Still, that bears monitoring…because each of the last three negative weekly MACD crosses has been followed by a significant decline in the index. (First chart below.)

The NDX Nasdaq 100 presents a somewhat different picture. The index rallied back to its previous highs before reversing lower last week in what proved to be a fairly significant decline. Even so, it remains much closer to its recent highs than to its 2026 lows…so we are not yet prepared to sound any major alarm bells.

The weekly MACD on the NDX has also begun to flatten out, but only modestly. The greater concern is the appearance of an outside-down week…where the index posted a higher high, and a lower low, AND it closed below the previous week’s low. That pattern often signals exhaustion…and can mark an important change in trend….Therefore, if (repeat, IF) the Nasdaq 100 experiences additional weakness and breaks below its June lows (just above the 28,000 level), it would signal that the technical outlook has deteriorated in a meaningful way. (Second chart below.)

The Russell 2000 continues to be the strongest of the three major averages….The small-cap index recently generated a positive weekly MACD crossover…while simultaneously breaking above both its previous all-time highs from earlier this year and the uptrend line that began with the late-March lows. Those are two very encouraging technical developments that suggest momentum is beginning to build in the small-cap universe…..So, unless the Russell reverses sharply in the very near future, its recent breakout should continue to provide a constructive signal for this long-neglected segment of the market. (Third chart below.)

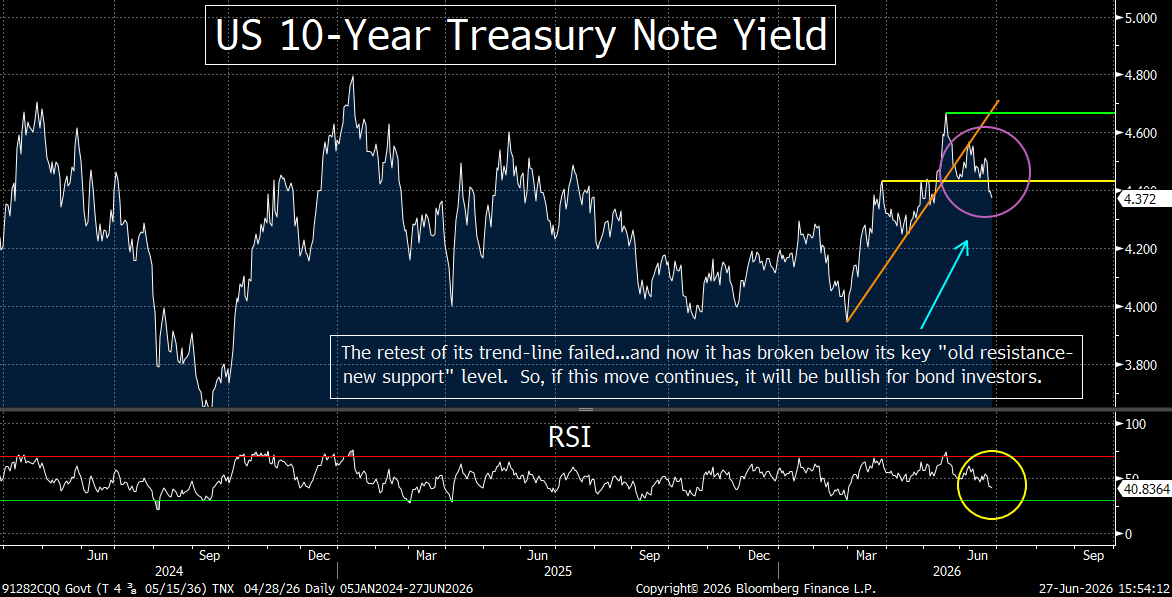

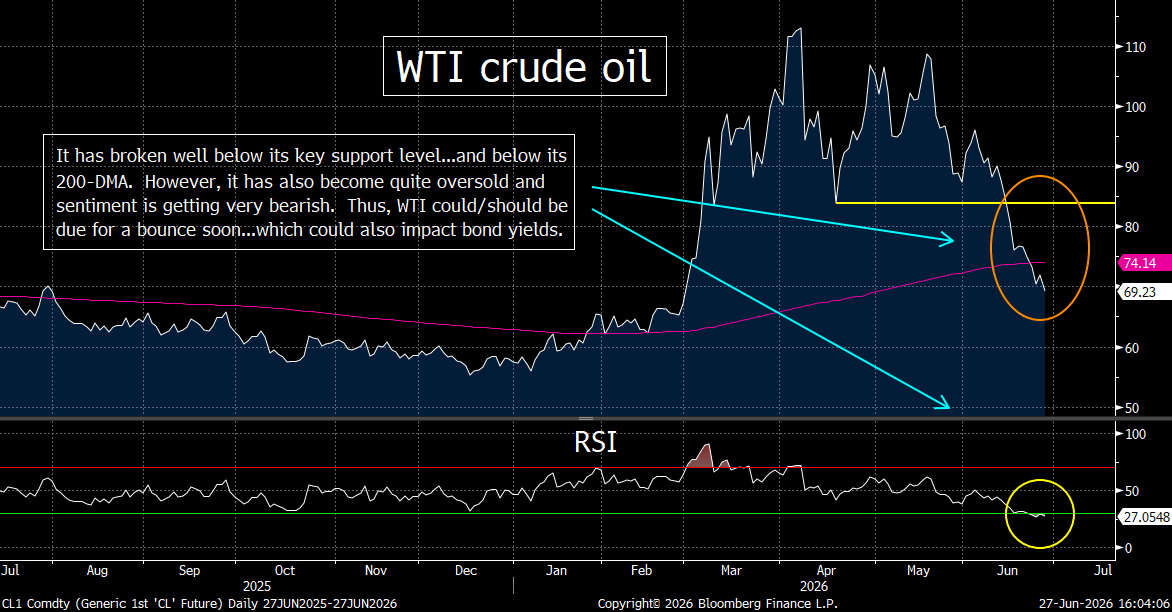

---6) Last week was quite a bullish one for the Treasury market…as long-term yields fell below some key support levels. We do need to point out, however, that crude oil is getting oversold…and sentiment surrounding this commodity has turned quite bearish. Therefore, it could/should be due for a bounce soon. That, in turn, could create some problems for bond investors…and thus they will want to remain very nimble in the days and weeks ahead.

The Treasury market’s biggest story last week was the sharp shift in the narrative surrounding long-term interest rates….One of the key catalysts was new Federal Reserve Chairman Kevin Warsh’s hawkish debut at his first FOMC meeting. Although a more hawkish Fed would normally be viewed as negative for bonds…the market interpreted Chairman Warsh’s strong commitment to fighting inflation as a credibility-enhancing development for the long end of the yield curve. Investors appeared to conclude that a Fed firmly focused on price stability would help keep long-term inflation expectations anchored…allowing the term premium to compress and providing support for longer-dated Treasury securities.

Another important factor behind the decline in long-term yields was the easing of geopolitical concerns surrounding energy prices. Oil prices moved lower during the week as negotiations between the United States and Iran appeared to make meaningful progress. The U.S. decision to grant Iran a 60-day license to sell oil on international markets also helped ease supply concerns…reducing fears that another inflationary energy shock was developing…..With lower oil prices easing inflation expectations, Treasury bonds found additional support.

Demand for Treasuries was also reinforced by market internals. The 20-year Treasury auction attracted very strong demand, signaling that institutional investors remain comfortable adding duration even after this year’s volatility. In addition, the latest Commitment of Traders (COT) report showed that asset managers continued adding long positions in Treasury futures…another encouraging sign that longer-term investors are becoming more constructive on the bond market.

Taken together, the combination of Chairman Warsh’s inflation-fighting credibility, easing oil prices, strong auction demand…and improving institutional positioning helped drive long-term Treasury yields lower last week…….For now, those factors suggest that the bond market is becoming increasingly confident that inflation risks may remain contained despite the Fed’s hawkish stance.

Looking at the chart on the US 10-year yield, you can see that last week’s decline means that it failed to push back above its trend-line from early this spring. After reversing at that line, it rolled back over and dropped below the key 4.4% level we have been talking about recently. (It’s “old resistance/new support” level). Therefore, this bodes quite well for fixed income investors going forward.

HOWEVER, we do need to point out that WTI crude oil is becoming quite oversold and over-hated. Yes, crude oil has fallen WELL below its key support level (its April lows)…and below its 200-DMA. That said, it has become very oversold on its RSI chart…AND we’d note that bullishness among futures traders fell to just 13% on Friday. Therefore, this oversold and over-hated commodity should be dure for some sort of bounce soon. That, in turn, could create some headwinds for the Treasury market……So, like equity investors today, fixed income investors will want to stay very nimble in the days and weeks ahead.

---7) The private credit market has slipped off the front pages in recent months, but that does not mean the underlying concerns have disappeared. In fact, several recent developments suggest that many of the same risks that worried investors earlier this year remain firmly in place. With this in mind, we will continue to monitor the developments in this market…as well as the share prices for the stocks of the private market companies.

Even though there have been a lot of renewed reports of the capping of redemptions in the private credit market, the attention that this market is seeing right now is quite low. However, when you look at the shares of the private market companies, you can see that there are still PLENTY of concerns among investors about this asset class.

Again, one of the biggest warning signs has been the growing number of private credit funds that are once again limiting investor withdrawals. Major firms including Blackstone, BlackRock, Apollo, Monroe…and most recently Ares…have all implemented redemption caps as investor withdrawal requests have exceeded available liquidity. In many cases, redemption requests have reportedly reached 10% to 18% of assets…while fund managers have limited withdrawals to just 5%.

The core issue remains the same: a mismatch between the illiquid nature of the underlying loans and the semi-liquid structures that have been marketed to investors. When investors want their money back…managers cannot easily sell loans without accepting significant discounts. As a result, redemption gates have become an increasingly common tool to manage liquidity pressures.

Valuation concerns also continue to cast a shadow over the industry. Due to the fact that many/most private credit investments do not trade regularly…determining their true market value can be difficult…and critics have described some of these valuations as “mark-to-myth” accounting…arguing that prices can remain artificially stable until a transaction suddenly reveals a much lower value. In some high-profile cases, loans that had previously been valued close to par (100 cents on the dollar)…have later been marked down DRAMATICALLY…highlighting the uncertainty surrounding the sector’s pricing mechanisms.

At the same time, credit fundamentals have weakened. Rising default rates…a growing number of distressed borrowers…and several well-publicized loan losses…have raised questions about the overall health of the asset class over the past 6+ months. Regulators are also paying closer attention to the industry…particularly given the growing interconnectedness between private credit firms, banks, and insurance companies. (Some prominent investors…like Hedge Fund manager…Lee Robinson, have even expressed concerns about insurance company exposure to the sector…and are positioning for potential serious stress in that area.

Also, the recent weakness in publicly traded private credit stocks has begun to raise yellow warning flags once again. While this may not be a crisis that comes to a head immediately…the risks remain significant. Investors should not mistake the lack of headlines for a lack of problems, because many of the structural challenges facing private credit remain unresolved.

We’d also note that the action in the stocks of the publicly traded private market companies continues to be abysmal. Yes, like almost all stocks, they bounced nicely in March and April. However, unlike the major indices, these stocks have ALL rolled back over in the past 6-8 weeks. None of them have taken out their Q1 lows, but the resumption of their declines is definitely raising some renewed questions about this asset class.

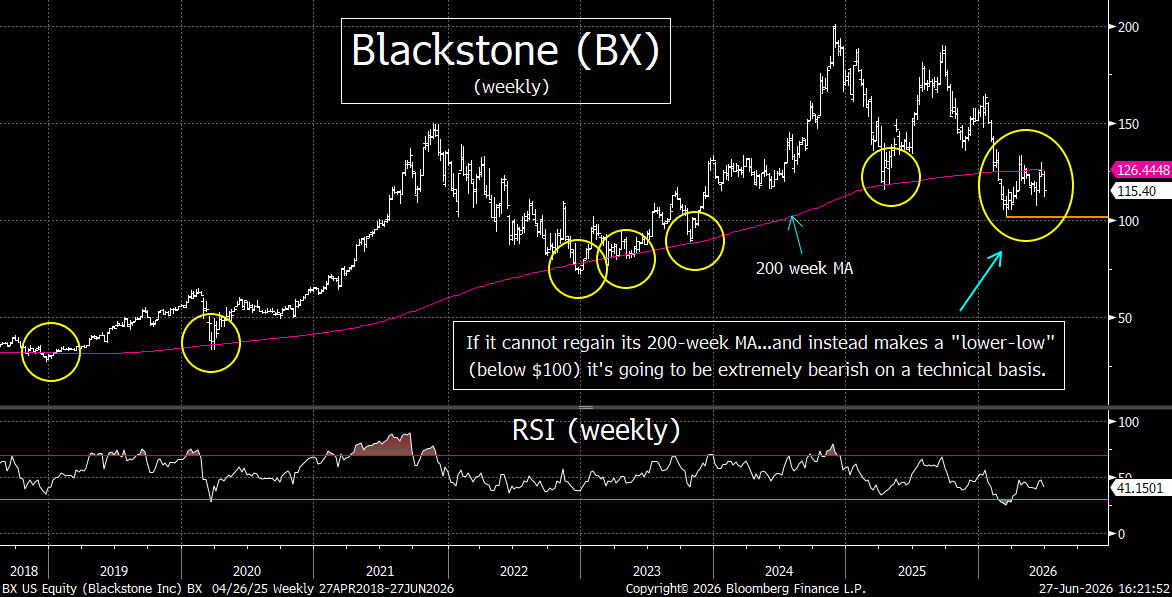

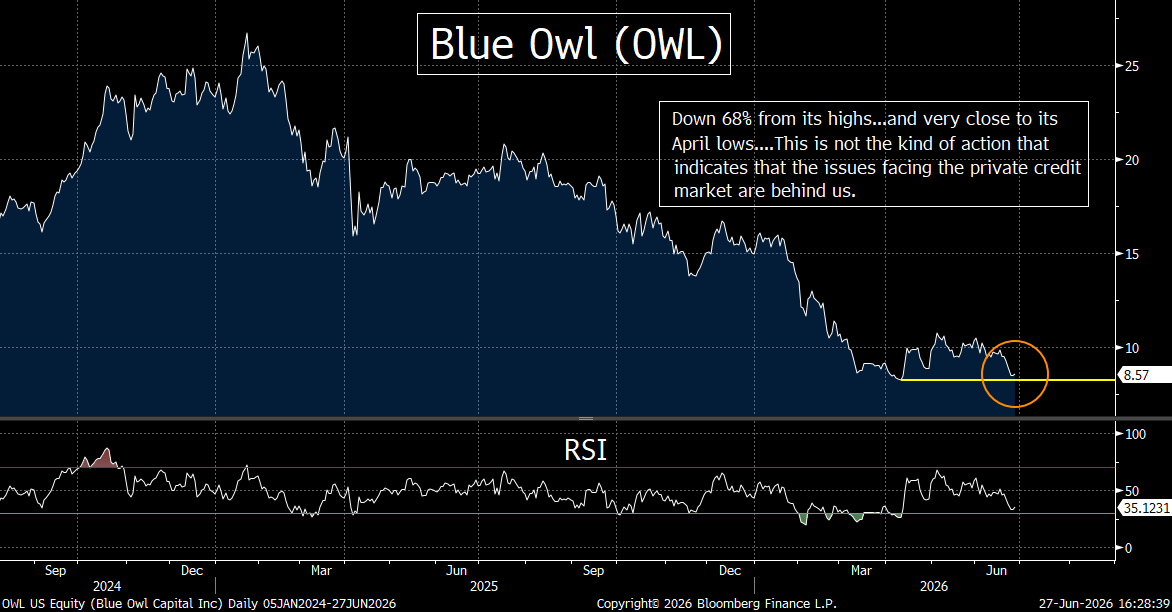

With Blackstone still 43% below its 2024/25 highs…Apollo 31% lower…and KKR 44% lower, these stocks have definitely been under serious distribution for a long time now. This is particularly true given that the S&P 500 has RALLIED almost 30% since those outsize declines in these private market stocks began! (We’d also point out that Blue Owl’s stock is down 68%...and is only 3% from its April lows…and they haven’t even revealed their most recent redemptions requests yet!!!)

We’ll finish this point by describing the charts on BX and OWL…..BX broke below its 200-week MA earlier this year. This was important…because that line had provided EXCELLENT support for the stock for MANY years. It has since tried to bounce back and retake that line several times, but it failed once again last week. Therefore, if (repeat, IF) it continues to decline…and takes out its 2026 low (of $100)…thus giving it a key “lower-low” (after failing to regain its 200-week MA), it’s going to be very, very bearish on a technical basis. More importantly, it’s not going to be good for the outlook for private credit either. (First chart below.)

As for OWL, this stock has rolled back over quickly…after a very feeble bounce…and it is now close to its April lows. (No wonder the Co-CEO sold his stake in the Washington Commanders.) That might sound like we’re being wise guys, but the fact that he sold that stake IS something that is quite telling to us…particularly given how poorly the stock acts……Either way, if it breaks below its 2026 lows in any material way, it’s going to be another red flag for the private credit market.

---8) Bitcoin had another rough week last week…as it dropped below the key $60 level in a slight way a few times. Whether it can bounce off this level soon in a substantial manner…or falls below that line in s significant way…is going to be CRITICALLY important for this asset class as we move through the rest of the summer months.

Bitcoin remains at an important crossroads…with both encouraging long-term developments…and meaningful near-term challenges shaping the outlook. On the bullish side, regulatory clarity appears to be getting closer as Congress is expected to pass a crypto market structure bill that would provide clearer rules for platforms engaging in digital assets. Such legislation could reduce uncertainty and encourage broader institutional participation over time. In addition, the institutional infrastructure built during the last crypto boom has largely held up well despite the recent downturn. Bitcoin ETFs, custody providers, and trading platforms remain firmly in place…while many long-term holders have stayed remarkably resilient.

Historically, periods when Bitcoin has suffered declines of roughly 50% have often created attractive buying opportunities for patient investors. Furthermore, Wall Street firms continue to invest in the infrastructure surrounding digital assets…reinforcing the possibility that Bitcoin remains an important part of the future financial landscape.

However, there are also reasons for caution……Retail investors, who were a major force behind previous rallies, have largely shifted their attention elsewhere…particularly toward high-growth AI and technology stocks. Bitcoin ETFs have experienced notable outflows…suggesting investor enthusiasm has weakened. (Last week was the 7th week in a row of outflows.) The cryptocurrency has also shown signs of decoupling from the equity market…raising concerns that it may not benefit from broader stock market strength. Finally, the long-term threat posed by advances in quantum computing continues to generate debate about future security risks. As a result, Bitcoin’s outlook remains balanced between promising structural progress…and lingering demand concerns.

From a technical standpoint, the outlook has become increasingly concerning. Earlier this year, Bitcoin broke below the neckline of a significant head-and-shoulders pattern near the $80,000 level. Although the cryptocurrency staged an impressive rebound during March and April…that rally ultimately failed when it retested the former neckline in May. The inability to reclaim that key resistance level reinforced the bearish implications of the pattern.

Since then, Bitcoin has rolled over once again and is now testing support near $60,000…which corresponds to the lows established during the first quarter. This level is extremely important. If Bitcoin breaks below $60,000 and establishes a “lower-low” (beneath its March trough)…it would confirm a more significant technical breakdown following the earlier head-and-shoulders violation. Such a development would likely signal additional downside ris…and could trigger a further deterioration in investor sentiment.

With all of this in mind, Therefore, the $60,000 level represents one of the most critical technical battlegrounds in the cryptocurrency market today…and is something investors should watch VERY closely in the weeks ahead.

---9) Summary of our current stance………..We definitely agree that the fundamental backdrop for the stock market does remain constructive in several important ways…which is why it would be premature to declare that this fabulous bull market (which we believe has become a bubble) is definitely on the cusp of coming to an end…..At the same time, we are becoming increasingly concerned that the recent action in the market is beginning to signal that a meaningful correction could be on the horizon…..While the long-term trend remains positive, the number of items on the bearish side of the bull-bear ledger are starting to grow.

On the bullish side, the biggest positive continues to be earnings. At the beginning of the year, Wall Street was expecting roughly 14% earnings growth for the S&P 500. Today, consensus expectations have climbed into the mid-20% range…and although that growth remains heavily concentrated in a relatively small number of companies, it has started to broaden out somewhat, which is an encouraging development. The AI spending cycle also remains remarkably resilient. Micron’s latest earnings report and forward guidance reinforced the view that hyperscalers are continuing to spend aggressively on AI infrastructure…suggesting that the investment boom still has further to run.

Lower energy prices are another welcome development. Crude oil has fallen sharply since the agreement to reopen the Strait of Hormuz…and now stand at their pre-war levels. This is easing inflation concerns…and helping long-term Treasury yields drift lower. No, interest rates have not declined nearly as much as oil prices…but any continued moderation would provide additional support for equity valuations.

The U.S. consumer has also proven far more resilient than many expected. Despite ongoing financial pressures, Friday’s University of Michigan consumer confidence data surprised to the upside…suggesting household spending may remain supportive of economic growth…..Finally, we’re beginning to see encouraging signs beneath the surface of the market. Small-cap stocks have started to outperform…and there has been some nice rotation into industrials, materials, healthcare, and biotechnology (which we predicted would take place)…..If that broadening trend continues, it would strengthen the overall foundation of the bull market.

Nevertheless, we continue to believe we are operating within a stock market bubble. That does not necessarily mean the bubble is about to burst…but history shows that when it eventually does, the decline can be both swift and painful. More importantly, we’re beginning to see some cracks that deserve close attention.

Broadcom’s earnings report a couple of weeks ago was particularly noteworthy. The company failed to raise guidance…and warned that margin growth could begin slowing. When you combine this with declining token prices and lower GPU rental prices…these developments raise legitimate questions about whether AI demand is beginning to normalize…..We’re also seeing AI business models gradually shift from subscription-based pricing toward pay-as-you-go structures. This is causing enterprise customers to become more cost-conscious. While AI spending remains elevated…investors are increasingly asking whether the eventual return on investment will justify the enormous capital expenditures being made today.

Meanwhile, valuations remain extraordinarily stretched by virtually every historical measure…particularly price-to-sales and price-to-book ratios. Market leadership also remains exceptionally narrow…a condition that has frequently characterized major market tops. Narrow leadership often reflects investor confidence in only a handful of momentum stocks rather than confidence in the broader economy.

There are also several macro risks that cannot be ignored. Geopolitical tensions remain elevated despite the recent improvement in oil markets. The Federal Reserve appears increasingly hawkish…and Chairman Waller has indicated that policymakers are placing less emphasis on supporting liquidity through Treasury bill purchases…by stating in their release that their RMP program will no longer be automatic.…..If the Fed put is indeed farther out of the market than investors have grown accustomed to…financial conditions could tighten more than many expect. At the same time, any effort by the Bank of Japan to defend the yen could disrupt the global carry trade and remove another important source of market liquidity.

Adding to these concerns are signs of stress emerging in parts of Asia. Questions surrounding AI demand have surfaced not only through Broadcom but also among memory suppliers such as SK Hynix…while South Korea’s increasingly fragile stock market could prove to be an early warning sign (a “canary in the coal mine”)…….Investors continue to believe that hyperscalers will ultimately earn attractive returns on their AI investments, but that assumption is beginning to face greater scrutiny.

For now, the music is still playing…and investors continue to dance. However, if we begin to see more meaningful evidence that AI demand is slowing…while global liquidity simultaneously becomes less abundant…the market could face a very difficult combination. Those are the developments we will be watching most closely in the days, weeks, & months ahead.